Lately, the troubles with tariffs are on everyone’s mind. Are they on? Off? On again?

What and who do they apply to? Are they inflationary? Recessionary? Do they make US manufactured products more appealing?

What does all this mean for my investment portfolio?

The new Trump Administration, like it or not, likes to move fast and seems to course correct every day, even multiple times within the same day, with policy announcements, revisions, executive orders, and more. And there’s no better example of this need for speed than the variety of tariffs being announced, implemented, delayed, and modified daily.

President Trump has indicated that he plans to put immediate tariffs on various imports from Canada, Mexico and China, effectively raising the cost of importing at least some goods from those countries. Of course, those countries are threatening a set of retaliatory tariffs on US exports into their markets. The President has also indicated that another round of tariff announcements will come in April and will include European countries, as well.

One thing is clear: Tariffs, no matter how carefully messaged, have the effect of immediately increasing costs for someone. And those costs will likely be borne, at least in part, by consumers who will be asked to pay higher prices. Companies may decide to absorb a portion of the costs of the tariffs and accept lower profit margins and earnings, as well. President Trump alluded to this reality of higher prices and market volatility in his March 4th speech to a joint session of Congress when he said, “We may have in the short term, a little pain and people understand that.”

It may be that while everyone understands it, not everyone thinks it is worthwhile. JP Morgan’s Chief Global Strategist, Dr. David Kelly, had this to say about tariffs, “The trouble with tariffs, to be succinct, is that they raise prices, slow economic growth, cut profits, increase unemployment, worsen inequality, diminish productivity and increase global tensions. Other than that, they’re fine.” He probably won’t be invited to Mara Lago anytime soon.

The unpredictability of these tariff policy announcements and subsequent adjustments makes it very difficult to predict how much economic pain ultimately will be experienced for how long. Nor can we foretell which companies and countries will be most affected. Investors and, by extension, the markets, made up of investors, don’t like this kind of uncertainty. This has been evident in the upward price trend of the VIX index, which is intended to measure the volatility of the US stock market. The index rose over 88%, from 14.77 to 27.86 between Valentine’s Day and March 10th.

In the big picture, though, long-term investors should keep in mind that this recent threat of tariffs is just the latest example of the many circumstances that have always left investors wondering, “But what does it mean for my portfolio? Am I going to be ok?”

Investors asked the same questions when President Trump was first elected in 2016, and again when he implemented tariffs on foreign steel and aluminum in 2018. We couldn’t stop asking these questions in 2020, as the world grappled with COVID-19. We asked the questions again when President Biden was elected and then again when Russia invaded Ukraine in 2022. And when inflation hit 9%, we asked the questions again as the Fed took actions that raised short-term interest rates from virtually zero to over 5% in 2022 and 2023. More recently, we asked the question when Israel retaliated against Hamas over the terrorist’s violent incursion, and again when President Trump was re-elected in 2024. When we stop and think about just the last ten years, it has been one seemingly seismic event after another. While the previous list is not a complete one, markets around the world have positively rewarded investors over the last ten years, with US markets clearly leading the way.

What should an investor be doing in response to this latest round of uncertainty?

At the risk of sounding simplistic, diversification is still the best answer to protecting your portfolio from both known and unknown threats, foreign and domestic.

The benefits of diversification include avoiding extreme losses that could come from being overinvested in the wrong thing at the wrong time. Another less talked about benefit is the increased likelihood that a portfolio will own and benefit from the next set of winners, including those unexpected winners who either had been losing or were simply off the radar. A third benefit is the lowering of portfolio risks, including volatility and a lack of timely liquidity.

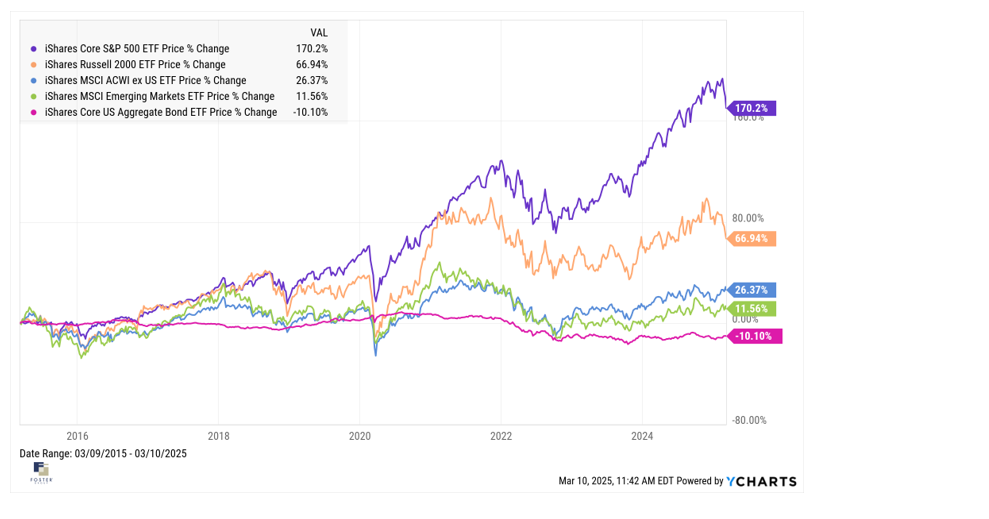

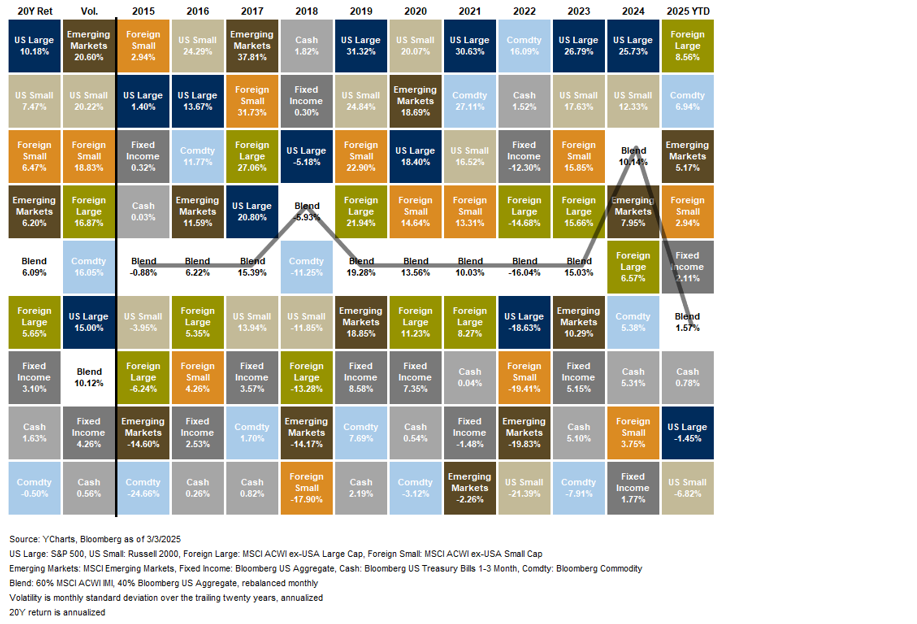

So far, 2025 has not looked like 2024, in terms of winners and losers. If an investor was only invested in US large and small company stocks as of March 10th, 2024’s two winningest asset classes, they would have found themselves wondering if they would have held the two worst performing major asset classes of 2025. After years of underperforming US stocks, foreign large company stocks have surprisingly been the best performing asset class of 2025, but it’s still early. Still, the stocks of large foreign companies were up almost 7% while the S&P 500 was down over 4% for the year as of Monday, March 10, 2025.

Here’s the basic message in favor of broad diversification: If you don’t know what is coming in terms of global economic or geo-political events (whether positive or negative), you want to be invested in things that are different from one another. In plain language, you don’t want all of your eggs (now more expensive thanks to Avian flu) in one basket, because you don’t know which basket will do well or poorly as circumstances change. In this case, the full reality of tariffs to be implemented is many months from being known. The full impact could be even further down the road.

So, instead of trying to invest in only one or two of the highest returning things, like the best stocks, the best country, or the one sector that might go up the most, you should want to own things that go up even when other things are going down. You should be fine with owning things that may go down while other things are going up.

In statistical language, you want to own a portfolio of assets, all with positive expected returns, but which are not highly correlated. Ultimately, all the asset classes you invest in should have positive returns; they’ll just realize those returns on different timetables. This means that your portfolio, while never being the best performer compared to the single best asset class for the period, will also never be the worst and will have a level of volatility, the thing that feels like risk, that is lower.

Why does diversification work for investors?

It has to do with the statistical concept of correlation.

Two assets are perfectly correlated when they both go up or down at the exact same time and to the exact same degree. Perfectly correlated assets have a correlation coefficient of 1. Statistically, the second asset adds no diversification benefit to the first.

Assets that are perfectly negatively correlated have a correlation coefficient of -1 and provide absolute diversification, in effect, cancelling out each other’s returns.

If the correlation coefficient between assets is close to 0, it means the two have return patterns that are impossible to predict, based on what either one is doing. They both may go up or down at the same time, or one may go down while the other is rising. And the rate at which they may be rising or falling is likely different. Assets that are non-correlated provide real diversification benefits.

In the real investment world, most pairs of assets turn out to be positively correlated to some degree, in part, because they should all have long-term positive expected returns.

Historically, the returns of stocks and bonds have had a very low correlation to each other. The Russell 1000 index of US large company stocks and the Bloomberg US Aggregate Bond Index have had a correlation of around .22 since 1988. Short-term bond returns have an even lower correlation to stocks. The ICE Bank of America 1-5 year US Treasury Note Index has had a negative correlation of -.01 with the Russell 1000 since 1988. That very slight negative correlation coefficient doesn’t mean short-term treasuries can be relied on to always go up when stocks go down, but they are very likely to perform differently than stocks.

Usually, bonds, and especially short-terms bonds, do well when stocks are under duress. I use the word, “usually,” because in 2022, both stocks and bonds declined precipitously as the Fed aggressively raised interest rates to fit inflation, reminding us that very few things aside from death and taxes are sure things. But this exceptional year doesn’t invalidate the norm, it just reminds us that anything can happen, especially when assets are not correlated.

Among stock asset classes, US large companies and US small companies have shown a positive correlation but one that is less than perfect. The correlation coefficient between them since 1988, has been around .85, which is fairly close to 1 but, again, showing a less than perfectly predictable correlation. These asset classes usually go up or down at the same time but not always and not always to the same degree. Foreign stocks show even less historical correlation with US large company stocks, with a correlation coefficient of about .75. All (three?) of these stock asset classes provide a diversification benefit to portfolios.

So, let’s go back to tariffs. What will happen next?

It’s unlikely that anyone’s crystal ball is clear on that. But what we can be confident about is that, after the uncertainty of this round of tariff policies fade, there will be another issue that arises, and that issue will appear to be a threat to market stability and investor portfolios.

Now and in the future, portfolio diversification is like owning insurance. When we are always diversified, in times of relative calm, we may wonder if it is a good strategy, especially if our home market is the world’s return leader. But in times of unexpected volatility, like when sudden wildfires destroy neighborhoods, we experience the benefits of insurance, of having assets in neighborhoods that are not burning down. For investors, this includes owning assets like lower but positively returning short-term bonds, as well as assets, in recently unpopular neighborhoods, asset classes like foreign stocks, which, from time to time, take over market leadership.

Tariffs are just the latest reason why staying diversified helps create resilient long-term, goal achieving, portfolios. Diversification always helps statistically and in tough markets and uncertain times. It helps us feel a little better, too. We’ve seen things like this before, and we’ll certainly see them again. But a look in the rear-view mirror reminds us that markets have a way of adjusting to the current realities, political and economic, and providing patient and optimistic investors with positive returns.

Today, as much or more than ever, developing an educated optimism, in this case seeing the value of diversification, can serve as an antidote for anxious uncertainty, and that’s a financial perspective worth pursuing. If you’re not convinced that your current investment plan is effectively diversified, now is a great time to evaluate it. At Foster Group, truly caring for our clients means taking the time to learn what’s in their hearts and helping them pursue their goals. We’d be glad to take a look.