Market periods like these have a way of making virtually everyone ask, “Am I OK?” Are my portfolio and financial plan going to survive these latest seismic events?

This is especially true when the news swings hourly from “Everything is terrible” to “Everything is resolved”. An important aspect of any financial plan is setting up the portfolio to provide income when wages or other sources of income stop or are not enough to cover our planned and perhaps emergency spending.

A presentation that I saw a number of years ago forever changed my view on what matters most to investors, determining the right mix of growth assets (think stocks) and preservation assets (think bonds and cash). In the industry, this is called Asset Allocation. It is also a source of financial peace of mind during times of market turmoil like we are experiencing right now.

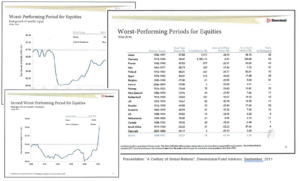

The presenter used a series of charts and graphs, like the one shown below. One of these charts is the “worst cases in history” table, showing how long and how low different global stock markets had plummeted over the last 110 years and how long they took to fully recover. The full peak-to-trough cycle, shown in inflation-adjusted dollars, was especially attention-grabbing. During market periods like the current tariff turmoil, I imagine many investors asked the same questions, “How long could this last and how bad could it get?” I think investors ask this question because they want portfolios and plans to survive even the worst cases.

Historical Worst Cases

Some of the historically worst cases for markets occurred during the World War II era. Japan saw their stock market decline by 97% from 1936 to 1947. It was 1969, or 22 years later, before the Japanese stock market broke even, reaching the same value, adjusted for inflation, as its previous peak in 1936. The French stock market declined over 87% between 1942 and 1950, only returning to inflation adjusted breakeven in the early 1980s.

The worst case for the US stock market was an eight-year period beginning in 1928, bottoming out in 1931 and then getting back to breakeven (in deflation adjusted dollars due to the Great Depression) by the end of 1936. For the global equity market, a capitalization weighted basket of all countries’ stock markets, the worst-case scenario, also started in 1928, bottoming in 1931, but returned to breakeven within seven years, one year faster than the US market alone. More recently, during the Great Financial Crisis, the US market took 59 months to go from peaking, October 7, 2007, to trough on March 3, 2009, to full recovery, April 2, 2012. Looking at over a century of stock market history is a good reminder about the importance of global diversification. Diversification spreads the risk and protects against any single asset or single country experiencing an almost unrecoverable disaster.

I believed then, and still do, that this historical perspective is crucial for investors evaluating their portfolio preparedness, no matter what the market environment. A good goal for a stock market investor is never to be forced to sell while stocks are down or declining. The simple formula for successful stock market investing is still to buy low and sell high. If you can’t hold stocks for the long-term, and by that I mean eight to ten years or more, it’s questionable whether you should be investing in them at all.

While growth is very important for long-term success, meeting your lifestyle spending requirements today, tomorrow, and for the rest of your life is just as important. In fact, a case could be made that it is even more important than growth. A good financial plan should tell you when you will need to withdraw money from the portfolio and how much is needed year by year, adjusted for inflation. For many of us, this cash flow need begins at or near retirement, because you now have financial obligations greater than all your other income sources, like wages and social security, combined. Based on those worst-case market scenarios we examined earlier, any amounts needed above income for at least the next seven years should be in some combination of cash and bonds.

Building Your Lifeboat to Weather Stock Market Storms

Here’s a simple example of how to check whether or not your portfolio is protected against long-term tariff turmoil or any other potentially long-term market crisis.

Let’s say that you plan to start withdrawing money from your portfolio for living expenses in 2026. Your financial plan shows that you’ll need $8,500 per month of income, with just over $100,000 per year of total expenses. $2,500 a month will come from social security, leaving $6,000 a month needed from the portfolio, about $72,000 per year.

If you don’t want to sell stocks while they are going down or before they have fully recovered, you can refer to that seven-year historical global market worst case and reasonably conclude that you need just over $500,000 in cash and bonds by January of 2026, seven years times $72,000 or $504,000. Ideally, you’d have started planning your portfolio allocation many years before retirement so that, during the seven years prior to needing income from the portfolio, you would have built up that $500,000 minimum.

Of that $500,000, we’d advise you to consider holding 1-2 years’ worth of spending, say $150,000, in cash. This could be money markets and/or high yield FDIC savings, for example. The remaining $350,000 could be invested in a diversified bond portfolio, with maturities varying from three to seven years. As always, the specifics of your situation may be different from these general guidelines, but this is a good starting point for evaluation.

Many people talk about portfolio allocation in percentages, but to understand your investment strategy in terms of preparation for and protection from bad markets, it can be far more reassuring to think in terms of dollars. You and I don’t spend percentages; we spend dollars and cents. And in this example, I am showing seven years of expenses isolated from stock market risk, because seven years is a historical worst case for a globally diversified stock portfolio.

This exercise describes what I call “your lifeboat,” the cash and bonds needed to keep your income afloat during a potentially long downturn in global stock markets. If you’re more conservative and don’t need to maximize your portfolio return to reach your goals, you may want to have more than seven years of cash flow in cash and bonds. Many people do!

From here we can zoom out and look at your entire portfolio and plan. Let’s say that you have a $2 million total portfolio divided between a 401(k), an IRA, and an after-tax brokerage account, along with checking and savings. Your seven-year lifeboat is just over $500,000. That represents about 25% of your total portfolio. Based on a set of conservative expectations, if your financial plan says that you need the expected return of a 60% stock/40% bond portfolio to safely reach your goals, you could choose to hold an additional $300,000 of likely lower returning but less volatile bonds. This extends your lifeboat to over ten years. If you like percentages, acceptable asset allocations for your portfolio would range between 75% stocks and 25% bonds and cash to 60% stocks and 40% bonds and cash. This range of allocations is expected to cover the contingency of a seven-year or longer stock market dip while at the same time providing enough stock market exposure to generate the longer-term return you need.

Two things in closing.

Recognize that our fear kicks into high gear in periods of big and/or sudden market declines. Behavioral psychologists have found that our brains respond more actively to what is happening right now than what we may know intellectually or believe to be true of longer-term market cycles. This is why many investors feel like they need to do something to respond to current markets. But, for an investor with a solid long-term plan and a portfolio that has seven to ten years’ worth of cash flow requirements already covered by cash and bonds, usually the best thing to do is hold your ground and live your plan.

Of course, you may want to review your plan and portfolio with your advisor for reassurance and just to confirm that nothing has changed. We encourage you to do that. Often a conversation and review of the facts serves to calm our inner doubts and allow us to get back to living our lives as planned.

Second, if you don’t have the amount of cash and bonds currently needed to cover seven years of spending and you are near or in retirement, you have a couple of options. One is to keep the portfolio as-is until equity markets recover and then have a plan already in place to work on funding your lifeboat. If you are three years or more from retirement, you could also redirect all current and future savings to bonds and cash. You could do this in your 401k by having all future contributions directed to bonds and cash while leaving your additional retirement accounts as is. If you are funding after-tax accounts, you can also direct new savings to cash and bonds. Finally, don’t forget to count any cash accounts you already have toward the total needed.

If you’re retired and your cash and bonds don’t cover seven years of future spending, find out how many years they do cover. The seven-year number corresponds to the worst case for global equities in the last 120 years. Hopefully, this current turmoil will not result in a worst-case scenario, and there are plenty of reasons to think it won’t. The economy and markets were in good shape prior to the tariff announcements and if the current uncertainty doesn’t drag on too long, there’s reason to think a recovery could happen quickly. The best recent example of a quick recovery is the US market in 2020, during the COVID pandemic. The entire peak to trough (the S&P 500 was down more than 33%), to full recovery took only four months! By comparison, this current drawdown saw US stocks find a trough, down just over 18% before recovering partially. And this cycle is still only a few months old. Of course, the future of markets, like everything else, are unpredictable. Anything can happen, good or bad, but there is reason for long-term optimism.

If you haven’t given much thought to the bonds and cash you may need to support your future spending goals, let the uncertainty you may feel right now act as motivation to take a closer look! Joe Wiggins put it this way, “We might know that equities can fall a lot in the short-term, but we won’t truly understand what that means until we feel it. We are far more likely to insure our house against flood risk after it has flooded – risk often only becomes real when we have experienced it.” Everyone is feeling “it,” the flood, the sudden market decline, right now. While we would not encourage sweeping changes to your portfolio, it is a great time to resolve not to be caught without a lifeboat when (not if!) the next market turmoil arises. At Foster Group, truly caring for our clients means taking the time to learn what’s in their hearts and helping them pursue their goals.