The $100,000+ Per Year Retirement Savings Opportunity – Cash Balance Plans

Many business owners are looking for more tax-friendly ways to save for retirement. The 2023 401k and profit-sharing plan limits allow individuals to save up to $66,000 ($73,500 with catch up) per year. Although sufficient for many, some company leaders would consider saving above and beyond their 401k and profit-sharing plan limits if they could.

Enter the cash balance plan.

What is a Cash Balance Plan?

Cash balance plans are the fastest growing type of IRS-qualified retirement plan in the United States1. Bank of America established the first plan in 1985. But popularity has increased since the 2006 Pension Protection Act (PPA) and additional clarifying regulations in 20142. Technically, they are a type of defined benefit plan, but they are referred to as “hybrid” plans, because they have characteristics of both a defined benefit plan (DB plan) and a defined contribution plan (DC plan).

Like a DB plan, the employer sets aside money and promises to provide a retirement benefit to each participating employee. Like a DC plan, each employee gets their own stated account balance. The U.S. Department of Labor provides more detail on how this works:

“In a typical cash balance plan, a participant’s account is credited each year with a “pay credit” (such as 5 percent of compensation from his or her employer) and an “interest credit” (either a fixed rate or a variable rate that is linked to an index such as the one-year treasury bill rate). Increases and decreases in the value of the plan’s investments do not directly affect the benefit amounts promised to participants. Thus, the investment risks are borne solely by the employer.”

How Much Can Be Contributed to a Cash Balance Plan?

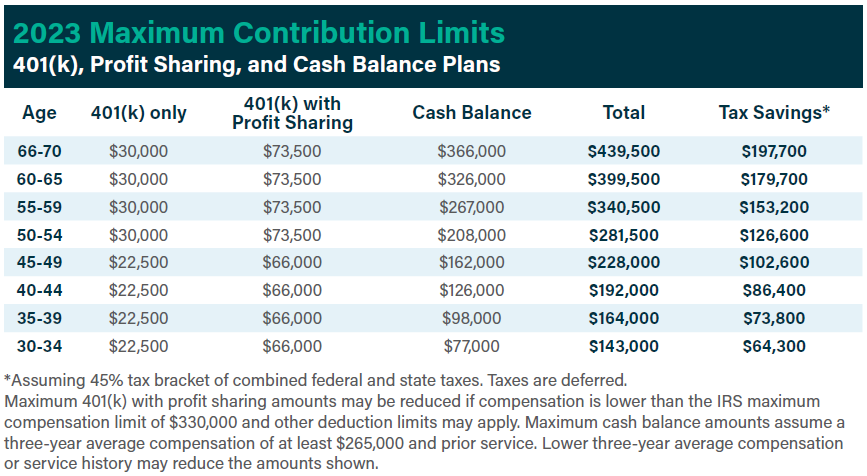

The simple answer is – a lot! To unlock the maximum allowable annual contribution, it is often necessary for business owners to make profit sharing contributions to employees. This helps them pass nondiscrimination testing and is a reason why cash balance plans typically work alongside a traditional 401(k) and profit-sharing plan. The table below shows the contribution limits for 2023.

Table Source: FuturePlan

Why Consider a Cash Balance Plan?

- High Contribution Limits: As seen in the table above, cash balance plans offer the opportunity to save a large amount toward retirement. For example, individuals between the age of 60-65 can contribute up to $326,000 to their cash balance plan in a single year! This could allow the business owner to “squeeze 20 years of savings into 103,” which might be helpful for professionals trying to catchup their retirement savings after paying off student loans or pouring extra money back into growing their business. (FuturePlan)

- Potential Tax Savings: Cash balance contributions are tax-deductible to the employer, which could lead to potential tax savings.

- Portable: When a participant leaves the plan or if the plan is terminated, the cash balance assets can be rolled into another qualified retirement account such as a 401(k) or individual retirement account (IRA).

- ERISA Covered: Like 401(k) plans, cash balance plans are covered under ERISA and are not subject to creditors in a bankruptcy.

- Retain and Recruit Top Talent: A cash balance plan is an employee benefit that could help in recruiting and retaining top talent.

Who Should Consider a Cash Balance Plan?

- In general, successful companies that are consistently profitable.

- Closely held businesses, medical groups, law firms, CPAs, and other professional services that have a desire (and cash flow) to save above the 401(k) and profit-sharing contribution limits.

Many business owners are looking for more tax-friendly ways to save for retirement. A cash balance plan could be the answer. They provide the opportunity to accelerate retirement savings and enjoy potential tax breaks. As business owners prepare for retirement, taking advantage of this “hybrid” plan could help them feel more confident about their future.

Sources: 1,22020 National Cash Balance Research Report, 3FuturePlan